Everything you need to know about HELOC Promissory Notes

Jennifer Park

Published: January 13, 2023 | Updated: April 13, 2024

When most people think of a promissory note, they think of a loan agreement between two individuals. But did you know that you can also use a promissory note to secure a home equity line of credit (HELOC)?

A promissory note for a HELOC is a credit agreement between the homeowner and the lender. The homeowner promises to repay the funds borrowed plus interest, according to the terms specified in the document.

This type of promissory note is often secured with collateral, such as real estate or other assets held by the borrower. The collateral serves as security for the loan and can help protect the lender if the borrower defaults on their payments.

The benefits of using a promissory note for a HELOC include:

- Flexibility to borrow larger amounts of money

- Access funds quickly and easily

- No need for you to liquidate or refinance other assets

As with any loan, there are some potential drawbacks as well. For example, if you do not keep up with your payments, your lender may be able to place a lien on your property or take other legal action against you. Additionally, the interest rate on a HELOC promissory note can be higher than with different types of loans.

Is There a Note for a HELOC?

Yes, there is a promissory note for a HELOC. The HELOC note outlines the terms and conditions of the loan agreement between the homeowner and the lender. It will detail how much money is being borrowed, what interest rate will be charged, when repayments are due, and other important information, such as any fees or penalties you may incur if the loan is not repaid on time.

HELOC loans differ from traditional bank loans, so it’s essential to read and understand the promissory note before signing. This is especially true for a balloon mortgage where the borrower is expected to make a single, large payment at the end of the loan term.

Can a HELOC Be Unsecured?

In some cases, a lender may agree to offer an unsecured HELOC. In this scenario, the borrower does not provide any collateral to secure the loan and is solely responsible for repaying the loan according to the terms outlined in the promissory note.

Unsecured HELOCs are generally more difficult to obtain, as the lender has no guarantee that borrowers will repay them. Due to the risk associated with the loan, lenders may charge a higher interest rate and require that the borrower has a good credit history.

You should also be aware that unsecured HELOCs typically have shorter repayment terms, so it is crucial to ensure that you can make the payments on time. Lenders can take legal action if the loan is not repaid according to the terms of the promissory note.

HELOC Promissory Note Example

A HELOC promissory note usually includes certain key terms, such as the following:

- Borrower and Lender Information: This refers to relevant details about the parties involved in the loan, including their legal names and addresses.

- Credit Limit: The credit limit is the maximum amount that the borrower can draw from the HELOC.

- Draw Period: The time frame during which the borrower can access funds from the credit line.

- Repayment Period: Details the length of time the borrower has to repay the borrowed amount after the draw period ends.

- Interest Rate: Describes the rate at which interest will accrue on the borrowed funds. This can be a fixed or variable rate tied to an index such as the prime rate.

- Payment Terms: These include how interest-only payments will be handled during the draw period and how principal plus interest payments will be handled during the repayment period.

- Fees and Penalties: Clauses on fees and penalties outline any fees associated with the HELOC, such as transaction fees, annual fees, and penalties for late payments or early termination of the line of credit.

- Minimum Payment Requirement: This term indicates the minimum amount the borrower must pay on a monthly or periodic basis.

- Collateral: Confirms that the borrower’s home is used as collateral for the HELOC, which means the lender can foreclose on the property if the borrower defaults on the loan.

- Default Terms: The terms describe the circumstances under which the borrower would be in default and the legal actions the lender can take in response, including foreclosure.

- Change of Terms: The clause specifies conditions under which the terms of the HELOC can be modified by the lender.

- Governing Law: Indicates the state laws that govern the interpretation and enforcement of the promissory note.

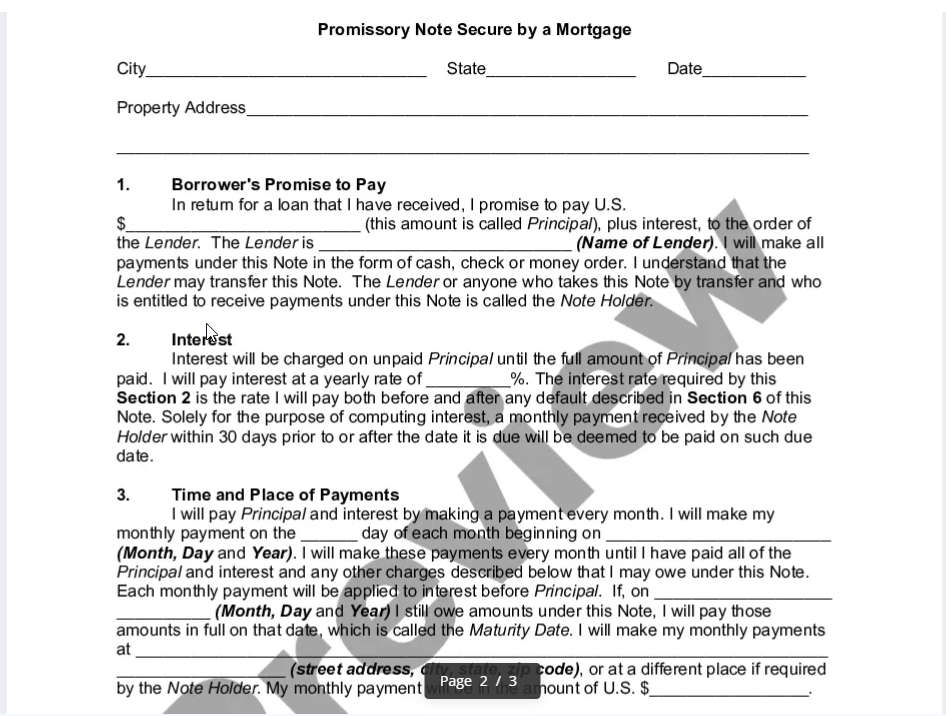

Below is a screenshot of a HELOC promissory note template available on the US Legal Forms website. You’ll notice that this template reflects some of the typical terms of a HELOC note.

Image Credit: US Legal Forms

Do You Need Tax Returns for HELOC?

For a Home Equity Line of Credit (HELOC), whether or not you need to provide tax returns can vary by lender and the specifics of your financial situation. Generally, lenders use tax returns along with other financial documents to assess your income stability and debt-to-income ratio, which are crucial factors in determining your eligibility and the amount you can borrow.

In some cases, particularly if you are self-employed or have a complex income structure, tax returns become even more essential to verify income. However, for salaried employees with straightforward financial situations, lenders might accept pay stubs and W-2 forms instead. It’s always best to check with the lender for their specific documentation requirements.

What Are Alternatives to Get a Loan?

Aside from a HELOC, several other options are available for borrowers who need to secure a loan. These include hypothecation, asset-based lending, or selling a note.

- Hypothecation. A hypothecation real estate loan involves using existing lender mortgage receivables as collateral for a loan. This lending is often used to finance working capital or asset accumulation. Hypothecating is a secure form of lending since the lender has collateral to back up their loan.

- Asset-based lending. This loan involves using assets such as inventory, accounts receivables, or equipment as collateral for a loan. Asset-based financing is often used by businesses that need quick access to capital.

- Sell a mortgage note. Selling a note is another option for borrowers who need a loan. This loan agreement typically involves the borrower selling the promissory note to an investor, who then collects payments from the borrower over time. The investor takes on all the risks associated with the loan, including any default payments.

These alternatives to a HELOC promissory note can be beneficial in certain situations, but borrowers should always read the terms and conditions of any agreements carefully before signing. To ensure that your interests are protected, it is best to work with an experienced financial professional who can help guide you through the process.

How Amerinote Xchange Can Help

At Amerinote Xchange, we understand the complexities of the mortgage and real estate markets. We specialize in buying residential and commercial mortgage notes, so we can help you navigate the process of getting a loan from start to finish.

Our knowledgeable staff will work with you to understand your financial goals and provide a tailored solution to meet your needs. We are committed to providing fast and efficient note-buying solutions so that you can get the loan in as little as 15 business days.

Contact us today to learn more about HELOC promissory notes and other mortgage note solutions.